Disability Insurance

Short-term and long-term coverage may help you take care of important expenses if you cannot work and earn an income.

Why Disability Insurance?

What you have now and your plans for the future largely depend upon your ability to work and earn an income. If you're like most people, you probably have insurance to protect your home, car, and savings — but do you have insurance to protect your ability to earn an income?

Wise Disability Insurance can provide protection against lost wages due to disability and help you cover important expenses when you cannot work and earn an income. You may use Wise Disability Insurance cash benefits for anything – to pay for groceries, housing, co-payments, and medical costs not covered by your health insurance plan.

Short Term Disability Insurance

Protect up to two-thirds of your income from an unexpected short term disability.

Bills and expenses don't stop when you become disabled, and insurance can help bridge the gap while you regain your ability to work.

Wise Short Term Disability Insurance pays cash benefits when you experience a covered disability and can't work. Benefits are paid directly to you regardless of workers' compensation, sick leave, or major medical insurance.

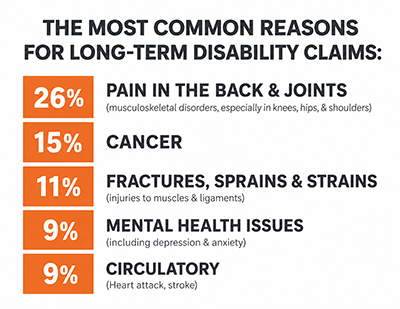

Long-Term Disability Insurance

Long-Term Disability Insurance typically begins where Short-Term Disability Insurance leaves off, providing benefits for illnesses or injuries that have longer recovery periods. Given the average duration of a long-term disability claim is two to three years1, the absence of emergency savings and rising medical costs can create a critical financial impact for many workers and their families.

Benefits from a Wise Long-Term Disability policy can last from several months to retirement age and help protect up to 60 percent of income when a covered disability occurs.

Consider the Facts

1 of 4

40%+

Disability Insurance FAQs

-

Why would I want short-term and long-term disability insurance?

Disability Insurance is a financial safety net for workers by helping to protect their income in the event of a disabling injury or illness.

Consider these questions:

- If you become disabled, how long could you pay bills and provide for your family with reduced earnings?

- How long will the disability benefit from your employer-sponsored insurance plan last?

- Do you have enough set aside to cover the additional expenses caused by a disability?

While a worker may have enough savings to weather a month's reprieve from work, a lengthy battle with cancer can quickly drain financial resources. The absence of emergency savings and rising medical costs today is creating a growing concern for many workers. Illness or injury can devastate personal finances. Supplemental income from Wise Disability Insurance can help when you can't work and still need to take care of yourself and your family.

-

How long do Disability Insurance benefits last and how much will I receive?

The length of time benefits are paid depends on your plan. Some policies provide coverage for a few months, while others may continue for several years or until you’re able to return to work.

When purchasing your insurance policy, you will have options. You can choose your benefit period (length), benefit earning percentage, and more.

-

How do I buy Wise Disability Insurance?Wise Disability Insurance is available as an individual policy and may also be available to you through your employer as a group policy.

Get a quote for an individual policy on our NTA Life web site.

Ask about Wise Disability Illness Insurance at work and learn more about this group benefit from Madison National Life.

Sources:

1. thecdia.org/how-disability-income-works, “How Disability Income Works,” 2026.

2. ssa.gov/pubs/EN-05-10029.pdf, “Disability Benefits,” 2026.

3. usnews.com/banking/articles/2026-financial-wellness-survey, “Survey: 43% of Americans Don’t Have Savings to Pay for a $1,000 Emergency,” 2026.